THERE have been many reported scams where property developers demand ‘Immovable Property Tax’ from property buyers.

THERE have been many reported scams where property developers demand ‘Immovable Property Tax’ from property buyers.

But rather than being based on the assessed 1980 value of the property as prescribed by law, these property developers base their illegal calculations on the price the buyer has paid for a property (the contract sum) as shown in their Contract of Sale.

Typically, the annual charge demanded is 0.4% of 50% of the contract sum. (E.g. For a property costing £200,000 the annual amount demand is calculated at: £200,000 ÷ 2 x 0.4% = £400).

Some developers demand even higher annual payments and some even add interest to their bill!

Other developers do nothing until the Title Deeds are issued. They then demand all the ‘unpaid’ taxes (plus interest) dating back to the time that the buyer purchased the property, often extorting money from buyers by using the threat of withholding Title Deeds to elicit payment.

In one case in which I was recently involved, these ‘unpaid’ taxes amounted to 50% of the property’s purchase price. Imagine buying a property for € 350,000 and then, some years later, receiving a demand from the developer for a further € 175,000 for ‘Immovable Property Tax’ before he’ll transfer Title!

Immovable property tax – an overview

Under Cyprus’ Immovable Property Tax laws 1980-2004 all property owners, regardless of whether they’re resident in Cyprus or not, are liable to pay an annual tax on the total value of all the immovable property (a term that relates to land and buildings) registered in their name.

Immovable Property Tax is calculated on the market value of the property as at 1st January 1980 and is paid annually the Inland Revenue Department.

Individual owners are exempt from this tax if the 1980 value of their property is less than CYP 100,000. As a result, you are extremely unlikely to pay (unless you have bought property valued in millions at today’s prices).

Every registered owner whose immovable property exceeds CYP 100,000 is required to submit a Declaration of Immovable Property (IR 301 and IR 302) and pay the respective tax every year before 30 September.

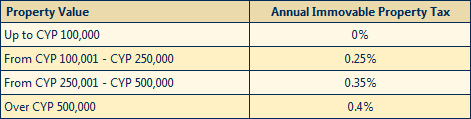

At the date of writing this article, Immovable Property Tax rates are as follows:

It should be noted that the nil rate Immovable Property Tax on property valued up to 100,001 only applies to natural persons. If you have set up a company (a legal entity) to own a number of properties, the nil rate does not apply.

Property buyers’ contractual obligations

Due to the delay in issuing Title Deeds, some developers are the registered owners of land banks whose value runs into many millions of pounds. It is the developer who is legally obliged to pay the Immovable Property Tax on these land banks, plus any interest due to late payment. But in their Contracts of Sale, some developers include a clause making buyers liable for Immovable Property Tax when they take delivery of a property rather than at completion (i.e. transfer of ownership).

Buyers in this situation must ask the developer to provide them with written evidence of the amount of Immovable Property Tax that has been paid to the Inland Revenue for the land on which the development has been constructed and the buyers share of that land.

E.g. If the development has been constructed on 100,000 m2 of land, and the buyer’s plot measures 500 m2, then the buyer should only pay 1/200 or 0.5% of the tax bill. So if the developer receives an Immovable Property Tax demand for € 10,000 the buyer should contribute € 50.

Buyers are warned not to pay a developer any Immovable Property Tax unless that developer:

- Supplies you with written evidence of the amount of Immovable Property Tax he has paid to the Inland Revenue for the land on which your development has been constructed.

- Provides you a written statement identifying your share of that land (see above).

- Provides a written invoice on the company’s letterhead for the agreed amount to be paid.

- Provides a written company receipt for the amount paid.

Reclaiming Immovable Property Tax from the Inland Revenue

Once buyers receive their Title Deed they may apply to the Inland Revenue, using Form IR 314, to reclaim any overpayment of Immovable Property Tax paid by the developer on their behalf. Buyers should take the completed Form IR 314, together with:

- Copy of the Title Deed of the property.

- Receipt issued by the Land Registry when the Contract of Sale/Sale Agreement was deposited for Specific Performance.

- Copy of the Contract of Sale/Sale Agreement.

- Receipt(s) issued by the property developer confirming the Immovable Property Tax paid.

to their local Inland Revenue Office.

Buyers should note that:

- Tax refunds resulting from overpayments exclude any interest charges that may have added for late payment.

- The 1980 value of their property (the value on which Immovable Property Tax is calculated, which will include the value of the land plus the value of the dwelling) will be assessed by the ‘Valuations Desk’ at the Land Registry at the time their Title Deeds are issued.